Recently, a new trend has emerged among the land of biotech initial public offerings (IPOs): the bigger the better. In December of 2018, Moderna Therapeutics set an industry record by raising $604 million for its IPO, giving the company an initial market capitalization of over $6 billion. Other companies such as Gossamer Bio and Adaptive Biotechnologies have since followed in Moderna’s footsteps with large IPOs of their own. It is tempting to stick to names like these when investing in the biotech IPO market. But, does bigger really mean better? We are going to travel back in time and invest a hypothetical $100 in several biotech IPOs, both big and small, and see what that investment is worth today. Will we find the sweet spot for biotech IPO investing? Let’s explore together.

By: Matthew Rojas, Biotech Financial Analyst

Range of IPO Offerings:

When companies IPO, they are grouped into categories according to the value of their market capitalizations. Nano-caps, a.k.a. “penny stocks”, have market caps of below $50 million and are generally considered the riskiest. Next up are micro-caps, which have market caps between $50 and $300 million; these companies are generally less risky than nano-caps but still exhibit a high degree of volatility. Then, there are small caps or companies with market caps between $300 million and $2 billion that have room for growth opportunities. After small caps are mid-caps, which are companies with market caps between $2 billion and $10 billion that are known for having more stability. Following mid-caps, large caps are companies with market caps of over $10 billion and represent the majority of the U.S. equity market. Lastly are the mega- caps: companies with market caps over $200 billion such as Apple (NASDAQ: AAPL), Amazon (NASDAQ: AMZN), and Facebook (NASDAQ: FB). For the remainder of this article, when referring to “smaller” biotech IPOs, what I mean are the nano-caps, micro-caps, and small caps that do not exceed $500 million. On the other hand, when referring to “larger” biotech IPOs, I am talking about mid-caps with market caps above $500 million and large caps. Since there has never been a biotech IPO considered a mega-cap, they will be excluded from this discussion.

The Small IPO Theory:

Just as many people claim that “bigger is better”, several individuals counter that belief with one of their own: “smaller is better”. The logic behind the latter theory is that smaller biotech IPOs potentially have more room for growth than larger biotech IPOs. Increasingly, many smaller biotech companies IPO without FDA approved product candidates. If people were to invest in these companies when they IPO and, in the future, one or more of their product candidates receives approval, investors’ earnings per share can skyrocket. Larger biotech IPOs also have room for growth; however, many believe that their growth is not as pronounced compared to smaller biotech IPOs. We will examine the large vs. small biotech IPO debate by examining how $100 investments in multiple IPOs over the last five years either grow or depreciate.

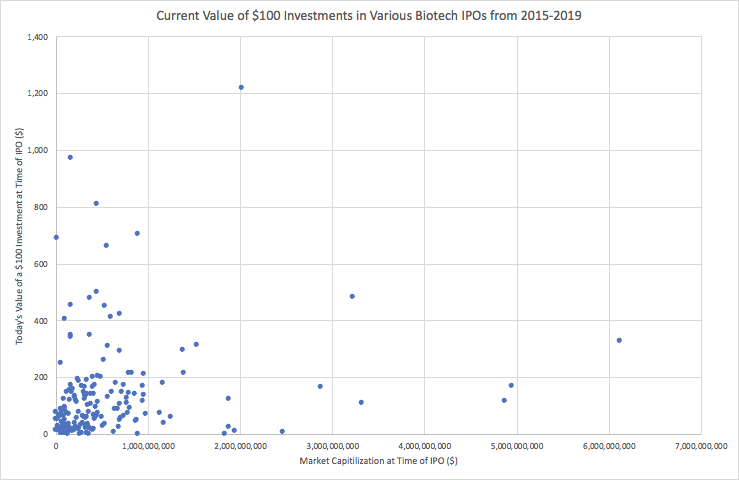

The Graph:

Each point on the scatter plot above represents a biotech company that IPOed within the last 5 years, 2014-2019, on either the NASDAQ or NYSE stock exchanges. There are a total of 175 companies on the graph gathered from the NASDAQ IPO database. The companies are arranged according to their market capitalizations on the date of IPO, listed on the x-axis, and today’s value of a hypothetical $100 investment in the company on the IPO date, listed on the y-axis. The IPO market capitalizations were obtained from the YCharts database, and the current values of the $100 investments in the various companies were derived using the percent change in share price from the date of IPO to the present. The reason for arranging the companies in this specific way is to discern if larger (>$500 million) or smaller (<$500 million) IPO market caps provide better opportunities for investment.

Potential Sources of Error:

Of the 175 biotech IPOs on the scatter plot, 117 or 67% of the companies have market caps below $500 million, and 58 or 33% of the companies have market caps above $500 million; therefore, smaller biotech IPOs are overrepresented in this data set. If more $100 investments grow in value for smaller companies compared to larger companies, this may be due to the larger sample size. Additionally, it is important to note that the IPO market cap is not the sole determinant of future success. Many factors play into a company’s success including but not limited to deals, FDA approval for product candidates, and mergers/acquisitions. Furthermore, if the market cap is found to be a significant factor in determining share price growth, it should be used as a data point among many others before an investment decision is made. Lastly, some of the IPOs, particularly those that IPOed in the beginning of the five year period, may have increased in value more because the $100 investments in those companies had more time to mature.

Findings:

Of the 117 companies that IPOed with market caps below $500 million, 42 or about 36% of them realized growth in the $100 investment at the time of IPO. On the other hand, of the 58 companies that IPOed with market caps above $500 million, 36 or 62% of them experienced growth in the $100 investment at the time of IPO. Even though the sample size of companies that IPOed with market caps above $500 million was smaller, this group performed much better in terms of return on investment compared to companies that IPOed with market caps below $500 million.

Having established that larger IPOs have outperformed the smaller ones over the last five years, it’s time to break down the larger IPOs into categories to see if we can find the sweet spot. There were 22 companies that IPOed with market caps between $500 and $750 million, and 13 or about 60% of them realized an increase in the $100 investments. Next, 17 companies had market caps between $750 million and $1 billion, and in 10 or about 59% of them, the $100 investment grew. Then, there were 11 companies that IPOed with market caps between $1 and $2 billion, and 5 or 45% of them saw the $100 investment increase. Lastly, there were 8 companies with IPO market caps between $2 and $7 billion, and 7 or about 88% saw the $100 investment increase — this appears to be the sweet spot. In all of these market cap categories besides the biotechs with IPO market caps between $1 and $2 billion, investors were more than 50% likely to receive a positive return on their investment.

Now, we are going to see how the groups within the smaller biotech IPOs, nano-caps, micro-caps, and some small caps, performed in terms of growth in the $100 investment. Of the 10 companies that IPOed with market caps below $50 million, 10% or one company experienced growth in the $100 investment. There were 65 companies that IPOed with market caps between $50 and $300 million, and of those companies, 20 or 30% of them realized growth in the $100 investment. Lastly, there were 42 companies with IPO market caps between $300 and $500 million, and 12 or about 29% of them experienced gains in the $100 investment. From this data, I would recommend steering clear of nano-caps because nearly all of them within the last five years decreased in value when looking at the $100 investment. When it comes to investing in micro-caps and small caps with market caps less than $500 million, some of them do have growth opportunities; I would just recommend researching the companies extensively before investing because they are significantly riskier than larger IPOs.

What to Look for in Smaller Companies:

There is room for opportunity when investing in smaller companies, you just have to know what to look for to find a successful candidate. The first thing to look for when researching is the company’s clinical pipeline. How far along are their clinical trials? Do they have multiple clinical trials or just one or two? If a smaller company only has two product candidates in pre-clinical trials, it could be years before they receive FDA approval; hence, these companies are very risky and one should stay away from investing. On the other hand, if the company has 5 product candidates and two of them are in phase 3 clinical trials, then this company is more likely to grow your investment.

Next, investors should examine the company’s recent news, deals, and current partnerships. Many companies have a “press release” section on their website where they post their most current news. It is always a good idea to scan that page for clinical trial updates and to see if they have made any deals with other leading biotech companies. If they have, then the company is more likely to be successful.

The last thing I recommend looking at is the company’s S-1 document, which every company has to file to the SEC to be listed on a public stock exchange. In this document, the company that wants to IPO addresses its risk factors, competitors, and even some consolidated financial statements. You don’t have to read the entire document, just search for individual words and phrases like “debt”, “risks”, and “competitive advantage”.

In Summary:

Today, I said we would answer the question, “Is bigger really better”? According to the data from 175 biotech IPOs over the last five years, the answer to that question is yes. Statistically, the initial $100 was more likely to grow when invested in the larger IPOs than the smaller ones. And, when looking at the $2 to $7 billion market cap range, investors were 88% likely to increase their earnings — this is the sweet spot. Does this mean you should blindly invest your money in any large biotech IPOs? No. It is always critical to research any company before investing, carefully looking at their pipeline, press releases, and S-1. Do our findings mean that you should steer clear of smaller biotech IPOs? Also no. There is still a lot of money to be made investing in smaller biotech IPOs; however, researching the company extensively before shelling out cash is essential. Overall, the biotech IPO space is filled with opportunity — definitely pay attention to the big players, but don’t forget about the smaller ones too.

More Stories

2026: THE YEAR THAT PATIENCE PAYS OFF?

WHO WINS IF AGING IS DEAD?

WHY IS AI STRUGGLING TO DISCOVER NEW DRUGS?